Come Visit us at our new site at http://donedam.com

April 14, 2008

Stylish Fire Safety for Your Home

Posted by dredam under Design, Gift Ideas, Misc, TipsLeave a Comment

Back in 2005 came the introduction of SnapAlarm, an award-winning optical smoke detector from FireInvent, and now the same Swedish company is taking fire protection a step further with its all-in-one Fire Safety Box.

The Safety Box is designed to provide complete fire protection in a single package, and it comes in six different versions tailored to different usage contexts. But the fire extinguishers, smoke detectors, fire blankets and torchlights included aren’t just ordinary versions of those items. Rather, they have been revamped for a modern, attractive look. The Safety Box Design, for example, includes fire extinguisher and Snap Alarm in black or white; black-and-white fire blanket in a modern, botanical design; plus an extra wall-mountable optical smoke detector. The Safety Box Exclusive, meanwhile, includes a chrome option for the fire extinguisher, while the Safety Box Kid includes a Snap Alarm in pink or blue and a fire blanket suitable for children. Pricing begins at $185 and versions for cars and boats are also available.

There will always be a need for functional products like fire protection devices, but there’s nothing to say they can’t be upgraded with a splash of color and design and sold at a similarly upgraded price.

March 23, 2008

Happy Easter from The Don Edam Group!

Posted by agentkelly under Events, For Fun, MiscLeave a Comment

Happy Easter, Happy House Hunting, and Speedy Spring Sales to all of our clients, friends, and family from all of us here at The Don Edam Group!!!

March 19, 2008

Minnesota Green: How to Save Our Environment One Reusable Envelope at a Time

Posted by agentkelly under Design, Green Living, Marketing, Misc, Tips | Tags: business, green, Marketing, Tips |Leave a Comment

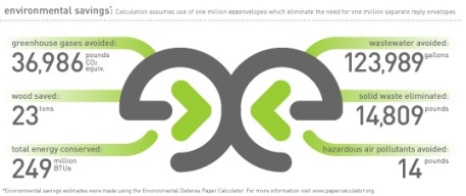

Minnesota is already known for being “nice”, but a local company called ecoEnvelopes is bringing nice to the world and attempting to turn corporate America green by helping businesses reduce their company’s environmental impact AND save money in the process.

After working for years to perfect the design and obtain the US Postal Service’s approval, ecoEnvelopes has developed an innovative line of reusable envelopes that simply zip open, allowing users to insert their response or payment and seal them up again just like a regular envelope. With 81 billion return envelopes being sent through the US mail each year, ecoEnvelopes stands to have a great impact on the environment by helping to reduce the estimated cost of envelope-excessive corporate America’s 1 billion pounds in greenhouse gas emissions and more than 71 trillion BTUs of energy.

Not only can everyone participate in environmental stewardship and feel good about their part in greening the mail (the envelopes are also made with up to 100% post-consumer recycled content!), but by eliminating the need to print, store, handle, insert, track and include a separate reply envelope, ecoEnvelopes can cut mail costs 15% to 45%, the company says.

Not a bad way to “green” our real estate businesses, I say! 🙂

March 18, 2008

First-Time Home Buying in 2008: 5 Reasons Why Now is a Good Time to Buy

Posted by agentkelly under Finances, Home Buying, Mortgages, News, Real Estate, Tips | Tags: Finances, first-time home buyer, homebuying, interest rates, Mortgages, Real Estate, Tips |Leave a Comment

With the constant barrage of negative media surrounding real estate these days, it’s no wonder that newlyweds and other first-time home buyers are putting their dreams of buying their first home on hold. But 2008 promises to be as good a time as any to buy your first home and here’s why:

It’s a buyer’s market

With foreclosures adding houses to a market already hungry for buyers and economists predicting that residential housing sales and prices will not pick up until 2009, sellers who need to sell are lowering prices and often throwing in additional incentives.

Perfect timing is rarely achieved

Although you should educate yourself and use caution when buying into a declining market, a buyer waiting for prices to hit absolute bottom, usually waits too long and then pays the cost of buying into a rising market with increased home prices. If you’re planning on staying put for a while, now is a great time to buy your first home because the market will eventually balance itself and turn once again to a seller’s market and when it does, your home’s value will increase too.

Interest rates are low

Recent Federal Reserve decisions have lowered interest rates yet again making the Federal funds rate drop to 2.25% (down from 5.25% a year ago) and the prime rate drop to 5.25%. And today a Bankrate.com index showed that the national overnight average for a 30-year, fixed-rate mortgage is being offered at 5.74% and a 15-year fixed at 5.09%, both of which are buyer-friendly rates.

Labor and materials are readily available

Even if you don’t qualify for enough financing to buy the home of your dreams due to tightening lending practices, it’s easier than ever to fix-up and maintain properties with the number of home improvement stores, tips, do it yourself classes and handymen readily available. And because new construction has slowed down in most markets and all trades that depend on it are eager for employment, buyers are likely to get better work, done faster and maybe a little cheaper in 2008 than at anytime in the future.

A need to sell makes sellers flexible

Remember, sellers who don’t need to sell right now generally don’t have their properties for sale. And those who do need to sell tend to be more flexible in negotiations, so buyers should consider proposing terms that ask sellers to help make the deal work beyond just lowering their price. Sellers may have the ability to finance part of the purchase price to make it easier on the buyer, they may be able to fix or replace something that needs updating, and they can always pay more than the customary share of closing costs and taxes.

Happy House Hunting!! 🙂

March 13, 2008

Green is the New Black at the 2008 Parade of Homes Spring Preview

Posted by agentkelly under Decor, Design, Events, For Fun, Green Living, Home Buying, Marketing, Misc, News, Real Estate, TrendsLeave a Comment

Green is the new black during this, the final weekend of the 2008 Parade of Homes Spring PreviewSM presented by Builders Association of the Twin Cities’ members.

This year’s Guidebook includes plenty of great Green articles to help us make sense of this growing movement and the homes in this year’s 14-home earth-friendly mini tour are built to showcase Green building practices, products and design, and many of them will host education seminars and other interesting events to give home buyers a better understanding of their Green options.

Some of the seminars that are taking place this weekend include: “Landscaping for a Green Community”, “Light up Your Home AND Your Energy Bill” and “Geothermal Heating and Cooling: A Systems Approach.” And I’m thinking about checking out an event with eco-friendly design expert, Jackie Kanthak, who will be will answering questions, giving green design ideas, and offering advice on the the hard to find eco-friendly products for the kitchen and bathroom.

Green or not, the homes on parade cover a broad spectrum of prices to fit the needs of every buyer, ranging from the lowest priced home by S.W. Wold Townhomes, Inc. in Cambridge, priced at $119,900, to the most expensive home by Stonewood LLC, located on Loring Drive in Minnetrista and priced at $2,950,000.

So come on out this weekend to take advantage of the longer days and beautiful spring weather that’s rolled our way, and peruse the preview parade!

For more information go to http://www.paradeofhomes.org.

Happy house hunting!!! 🙂

:: Kelly ::

March 11, 2008

A Fresh Perspective in Real Estate

Posted by agentkelly under For Fun, Home Buying, Home Selling, Marketing, Misc, Mortgages, News, Real Estate, Services, Tips, TrendsLeave a Comment

Greetings everyone!

I wanted to take a moment and introduce myself. My name is Kelly Carlson, Marketing Manager for the Don Edam Group, and I’m going to be contributing to this blog (and to the real estate industry in general) in the days to come, from a completely new and different perspective than your typical real estate professional.

Hoping to utilize a trifecta of my favorite hobbies (trend hunting, exploring new places, and trying new things), as well as tapping back into the service journalism and editorial voice that my U of M education once afforded me, my intentions are to keep you posted on all the latest news, statistics, tips, and trends in real estate and to scope out and share with you all of the food and dining, shopping and style, arts and entertainment, health, education, and local events that make our Twin Cities neighborhoods unique and fabulous places to live!

Although I am relatively new as a licensed real estate agent, I’m excited to know that the combination my background, work and educational experience, and personal interests can lend something new to the industry. While my expertise (& nearly a decade of experience!) lies primarily in promotions, marketing, and trend research, I also have 2 years experience as a credit analyst for a local mortgage services company and 4 years experience in title insurance research, giving me a range of knowledge and skill that can only add to our clients’ success.

I get a kick out of being a social anthropologist and spotting changes in consumer behavior, scoping out new trendsetting products and services, and just about any super-smart thinking on where our societies are headed at large. I look forward to developing new and innovative ways of marketing your homes and neighborhoods so that others can see why you called it “home” for so long, and I hope you enjoy the information I can share with you about the people, places, and events that form our great Twin Cities communities.

In the meantime, happy house hunting and speedy sales to all! ![]()

Kelly

March 10, 2008

New Contributor

Posted by dredam under Misc, News | Tags: Blog, new, The Don Edam Group |Leave a Comment

We’ve been quiet for a little while over here while we work on redesigning our blog and attempting to improve content. Helping me do that is our Marketing Manager, Kelly Carlson. Kelly will start to become a frequent contributor to this blog. I feel she’ll do a great job and should be able to comment on many things that I don’t have the expertise in. So, please welcome Kelly to the site!

Also, be on the lookout for a redesigned site in the next couple weeks. As always, you’re comments are greatly appreciated.

February 22, 2008

There’s really no sure way to avoid an audit. Most audited tax returns are selected for review either because the filer is part of a target group or because a computer program selects the return. The computer selects many returns randomly, but there are red flags that will draw the IRS’s attention.

The key is to minimize your exposure. Here are some suggestions from MSN Money on things you should try to avoid:

1. Math mistakes

The biggest reason people receive letters from the IRS is addition or subtraction goofs. Fortunately, math errors rarely lead to a full audit. Still, double-check your math before you send in your return.

And if you receive a letter from the IRS that says you owe them, check your numbers first. Sometimes, the IRS misreads one of your numbers, or the number is keyed incorrectly into the IRS computer. If it’s wrong, send a letter with a printout of your calculations.

2. Mismatched interest and dividend reporting

If the amounts reported in supporting documents don’t match the amounts on your return, you will get a letter.

There are lots of possible errors here. Sometimes, the IRS will enter the Form 1099 information into its computer and erroneously keystroke the income amount or the Social Security number of the recipient. If the income isn’t yours, get a letter from the bank or other payer and forward that letter to the IRS. If the amount is incorrect, send a copy of the Form 1099 mailed to you by the payer.

3. You’re on the IRS hit list

Those who receive much of their income in cash are traditionally on the radar screen of IRS agents looking for unreported income. Recently, the IRS has also pinpointed small-business owners and the self-employed in its bid to find more of the estimated $345 billion in uncollected taxes.

4. You’ve got a big mouth

Never brag about how you put one over on the IRS. Internal Revenue Service informers can earn a reward of between 15% and 20% of the additional tax collected, including fines and penalties and interest. Whistleblowers can file Form 211 or call the IRS hotline at 1-800-829-0433. Everyone else: Zip it, and keep your accounting strategies to yourself.

5. You’re exceptional

An IRS computer program compares your deductions to others in your income bracket and weighs the differences. This secret IRS formula, called the “DIF Score,” is used to select returns with the highest probability of generating additional audit revenue.

The IRS is coming

If you are facing an audit, don’t panic. An audit is merely a process where the IRS asks you to substantiate the numbers on your tax return. Here are some survival strategies:

Call your tax professional. Or get one. If the audit is simple – to prove your charitable and interest deductions, for example – you can do it yourself by mailing in copies of your substantiation. For all in-person audits, I strongly suggest professional representation.

Plan your taxes to preempt an audit. If, say, you have a huge medical deduction that you feel would increase your chances of being audited, attach copies of your medical bills to your return. The IRS computer will still kick out your return, but when a real person looks at it, the reviewer will recognize that you know the rules. This may actually reduce your odds of a full audit.

Keep records for three years. The IRS can audit you for three years after you file your return. In reality, however, most returns are audited within 18 months. This gives the IRS time to do the review and request the appropriate substantiation before the statute of limitations (usually the three-year period) ends.

Once the deadline has passed, the IRS normally cannot audit your return and your expenses are insulated from examination.

File at the last minute if you are concerned about a potential audit. It won’t hurt and might decrease your chances of being selected. The good news is, if you are audited one year with a refund or no change, it decreases your odds of being audited in subsequent years. In fact, if you are audited on the same items two years in a row with no additional taxes due, the IRS manual specifically recommends that they not audit you on the same items for a third year. Full Story

February 22, 2008

Foreclosure Filings Report: Hardest Hit Markets by State

Posted by dredam under Finances, Foreclosure, Mortgages, News, TrendsLeave a Comment

U.S foreclosure filings continued their upward climb in December, rising 97% from the previous year and 7% from the month before. Total foreclosures rose 75% in all of 2007.

According to MSN Real Estate’s latest report, hardest-hit markets were along both coasts, which experienced a more severe boom and bust in the latest cycle, as well as areas hard hit by auto-industry layoffs such as Michigan and Indiana.

The surge in foreclosures is expected to continue at this same pace until after the next wave of risky loans resets in the middle of 2008.

2007 foreclosure filings by state

|

Rate Rank |

State Name |

Total # of filings |

% chng. from 2006 |

% chng. from 2005 |

Total # of properties |

%Households |

|

1 |

Nevada |

66,316 |

215.12 |

758.68 |

34,417 |

3.376 |

|

2 |

Florida |

279,325 |

123.96 |

129.25 |

165,291 |

2.002 |

|

3 |

Michigan |

136,205 |

68.32 |

282.22 |

87,210 |

1.947 |

|

4 |

California |

481,392 |

237.99 |

681.95 |

249,513 |

1.921 |

|

5 |

Colorado |

71,149 |

29.96 |

140.12 |

39,403 |

1.919 |

|

6 |

Ohio |

153,196 |

87.93 |

207.35 |

89,979 |

1.797 |

|

7 |

Georgia |

99,578 |

31.07 |

118.43 |

59,057 |

1.566 |

|

8 |

Arizona |

69,970 |

150.91 |

160.7 |

38,568 |

1.516 |

|

9 |

Illinois |

90,782 |

25.29 |

94.3 |

64,310 |

1.25 |

|

10 |

Indiana |

52,930 |

11.31 |

73.57 |

27,980 |

1.027 |

|

11 |

Tennessee |

45,834 |

24.56 |

65.66 |

25,914 |

0.983 |

|

12 |

Texas |

149,703 |

-4.57 |

9.22 |

84,469 |

0.936 |

|

13 |

Missouri |

32,022 |

80.93 |

176.74 |

23,492 |

0.906 |

|

14 |

New Jersey |

53,652 |

34.06 |

52.75 |

31,071 |

0.902 |

|

15 |

Utah |

9,668 |

-25.87 |

-16.19 |

7,438 |

0.852 |

|

16 |

Connecticut |

23,470 |

100.05* |

111.38* |

11,860 |

0.833 |

|

17 |

Maryland |

25,109 |

455.26 |

388.41 |

18,879 |

0.83 |

|

18 |

North Carolina |

37,426 |

66.52 |

135.07 |

29,101 |

0.739 |

|

19 |

Mass. |

41,487 |

161.14 |

751.36 |

17,737 |

0.66 |

|

20 |

Idaho |

6,032 |

140.51* |

119.83* |

3,640 |

0.611 |

|

21 |

Washington |

23,705 |

27.95 |

59.47 |

15,184 |

0.573 |

|

22 |

Oregon |

10,746 |

12.25 |

56.76 |

8,461 |

0.543 |

|

23 |

Oklahoma |

13,594 |

-12.78 |

0.71 |

8,256 |

0.52 |

|

24 |

Virginia |

24,199 |

456.3 |

728.73 |

16,307 |

0.514 |

|

25 |

Minnesota |

13,615 |

127.11* |

506.73* |

11,557 |

0.513 |

|

26 |

Arkansas |

14,310 |

26.44 |

23.58 |

6,406 |

0.513 |

|

27 |

New York |

57,350 |

10.19 |

54.72 |

38,688 |

0.493 |

|

28 |

Alaska |

1,650 |

54.64 |

17.69 |

1,332 |

0.486 |

|

29 |

Wisconsin |

17,503 |

131.15* |

241.79* |

12,133 |

0.486 |

|

30 |

Nebraska |

3,971 |

30.88 |

91.84 |

3,636 |

0.474 |

|

31 |

Rhode Island |

3,241 |

153.80* |

7804.88* |

1,838 |

0.41 |

|

32 |

New Mexico |

3,893 |

-26.04 |

-46.55 |

2,994 |

0.357 |

|

33 |

Iowa |

7,404 |

114.92* |

251.90* |

4,103 |

0.314 |

|

34 |

Pennsylvania |

34,089 |

-11.07 |

18.98 |

16,379 |

0.302 |

|

35 |

Kentucky |

8,793 |

23.45 |

76.96 |

5,105 |

0.274 |

|

36 |

Montana |

1,378 |

29.27 |

52.6 |

1,150 |

0.268 |

|

37 |

Alabama |

7,903 |

81.76 |

83.07 |

5,572 |

0.268 |

|

38 |

Delaware |

1,430 |

225.00* |

342.72* |

999 |

0.266 |

|

39 |

South Carolina |

5,038 |

-27.56 |

-33.76 |

4,247 |

0.22 |

|

40 |

New Hampshire |

N/A |

N/A |

N/A |

1,238 |

0.212 |

|

41 |

Louisiana |

7,331 |

151.58* |

90.61 |

3,968 |

0.204 |

|

42 |

Kansas |

4,978 |

20.85 |

161.31* |

2,434 |

0.203 |

|

43 |

Hawaii |

1,270 |

88.71 |

-60.39 |

966 |

0.197 |

|

44 |

Wyoming |

497 |

21.52 |

99.6 |

356 |

0.151 |

|

45 |

Mississippi |

1,997 |

91.65 |

4.55 |

1,409 |

0.114 |

|

46 |

North Dakota |

308 |

74.01 |

86.67 |

250 |

0.082 |

|

47 |

West Virginia |

1,135 |

30.31 |

10.95 |

460 |

0.053 |

|

48 |

Maine |

N/A |

N/A |

N/A |

286 |

0.042 |

|

49 |

Vermont |

61 |

35.56 |

1.67 |

29 |

0.009 |

|

50 |

South Dakota |

N/A |

N/A |

N/A |

24 |

0.007 |

| District of Columbia |

800 |

607.96* |

393.83* |

777 |

0.28 |

|

|

— |

U.S. |

2,203,295 |

74.99 |

148.83 |

1,285,873 |

1.033 |

*Actual increase may not be as high due to improved or expanded data coverage in this state.